Skip to main content

Search

Search This Blog

all the days of our life

Posts

Showing posts from January, 2015

Show all

Posted by

Unknown

January 31, 2015

Financial Freedom: What Now?

Posted by

Unknown

January 13, 2015

Financial Freedom: Frugal Living

Posted by

Unknown

January 12, 2015

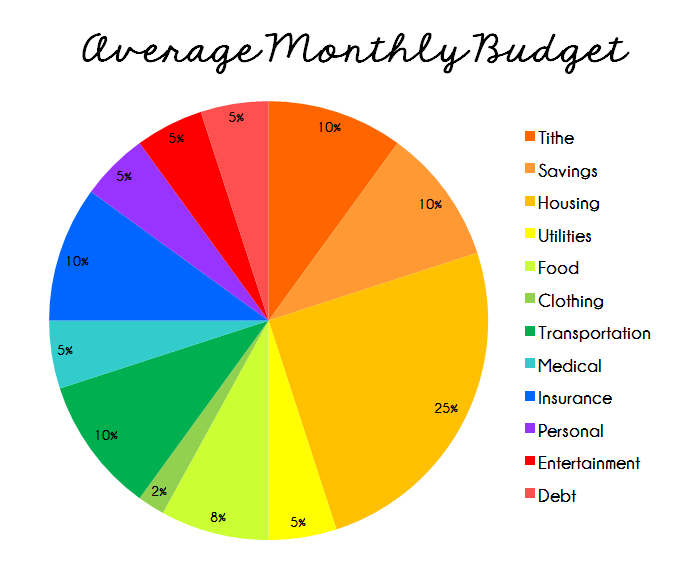

Financial Freedom: Budgeting

Posted by

Unknown

January 10, 2015

Financial Freedom: Financial Peace University

Posted by

Unknown

January 09, 2015

Financial Freedom: The First Step

Posted by

Unknown

January 08, 2015

Financial Freedom: Our Debt

Posted by

Unknown

January 07, 2015

Financial Freedom: Our History

Newer Posts

Older Posts

Home